The landscape of trucking in the United States is changing rapidly, and the driving force behind this shift isn’t on the highways, but rather in the trade policy offices in Washington, D.C. For independent carriers and large commercial fleets, understanding the evolution of tariffs on goods from China has gone from being a distant macroeconomic issue to a determining factor in the profitability of every mile traveled.

Tariffs are, essentially, taxes that a government imposes on goods imported from another country. By making foreign products more expensive, the aim is to protect domestic industry or exert diplomatic pressure on a trading partner. However, in a globalized economy, these tax rates generate a domino effect that directly impacts those responsible for moving supply chains: the transportation sector.

This journalistic investigation breaks down the real impact of tariffs from an analytical perspective, using indicators from federal agencies, data from industry organizations, and reports from economic research centers.

Effects of Tariffs on Routes and Cargo

The most immediate effect of tariffs on the U.S. economy has been the reconfiguration of international trade. According to official data from the U.S. Census Bureau, U.S. imports from China fell 40.7% in the first quarter of this year, reaching $60.87 billion compared to $102.66 billion in the same period of the previous year. This historic contraction has relegated China to fourth place among the nation’s trading partners, surpassed by Mexico, Canada, and Taiwan.

For trucking professionals, this statistical shift translates into a severe disruption of traditional transportation routes:

Loss of dynamism on the West Coast: The ports of Long Beach and Los Angeles in California, historical recipients of transpacific maritime traffic, have experienced notable fluctuations in container volume. This reduces the demand for drayage (local container transport from the docks to nearby warehouses) and intermodal services.

Boom in the Southern Corridor and the Texas Border: With Mexico consolidated as the main trading partner of the United States, land ports of entry such as Laredo, Pharr, and El Paso in Texas are registering record truck crossings. Demand has shifted toward routes in the Southwest and the Deep Interior (Midwest).

Volatility Phenomena (Frontloading): According to logistics analyses of the maritime and land freight sector, every announcement or threat of new tariff increases causes importers to accelerate their purchases to bring merchandise in before the tariffs take effect. This creates artificial peaks in demand for land freight, followed by prolonged periods of stagnation or “valleys” in cargo volume, hindering fleet operational planning.

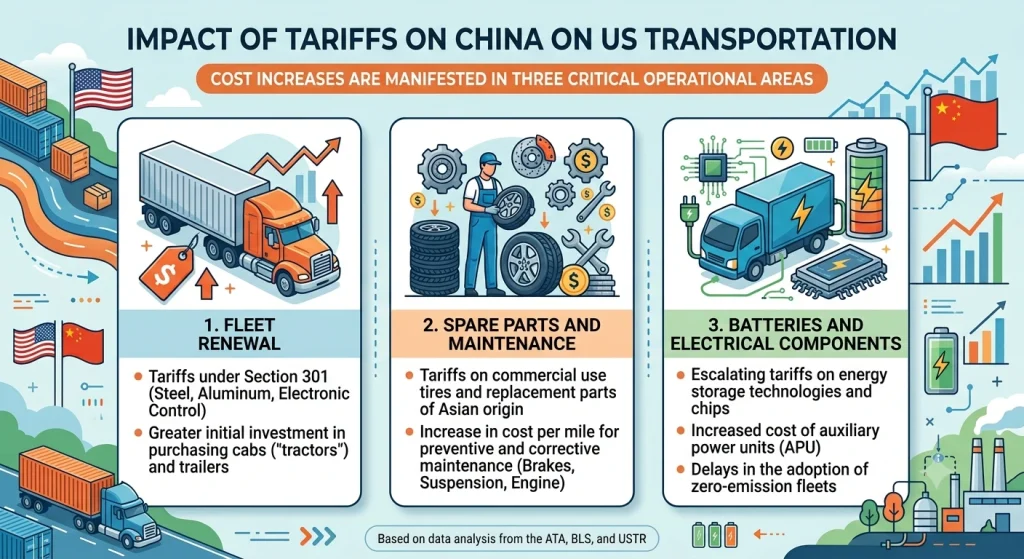

Additionally, modifications by the Office of the United States Trade Representative (USTR) under Section 301 have progressively increased tariffs on strategic Chinese goods, reaching 25% on steel and aluminum, 50% on semiconductors, and up to 100% on electric vehicles. As raw materials and intermediate technological components become more expensive, domestic industrial production faces higher costs, limiting the total volume of manufactured cargo ready for road distribution.

Tariffs and Higher Operating Costs

Beyond the disruption to cargo volume and origin, the transportation sector suffers the direct impact of tariffs on its own equipment. The structure of a Class 8 truck and its components depend critically on global supply chains that are currently under tax pressure.

The American Trucking Associations (ATA), the leading labor and business voice in the sector, has expressed its concern over rising input costs. According to the organization’s technical estimates, continued high tariffs on metals and essential components could increase the purchase price of a new truck by up to $35,000. This increase represents an indirect tax for trucking companies, making it harder for small operators, who form the backbone of the country’s transportation sector, to upgrade their equipment.

This scenario of high costs coincides with widespread inflationary pressures. Consumer Price Index data from the Bureau of Labor Statistics (BLS) show that prices for basic goods (excluding food and energy) have continued to rise (2.8% year-over-year in recent measurements), driven in part by import costs. For carriers, this means that while their operating costs rise, overall purchasing power shrinks, limiting their ability to negotiate higher freight rates with shippers.

In a fragmented market with historically tight margins, efficiency and strict control of variable costs become a true defense for the operator. The legal and tax environment continues to evolve; the ongoing legal battles regarding the Executive’s authority to impose emergency tariffs (such as the debates surrounding the International Emergency Economic Powers Act or Section 122) maintain a climate of legal uncertainty that forces fleet managers to continually revise their budgets. Tariffs, far from being a simple macroeconomic variable, are becoming the invisible factor that now determines the course of the road on American highways.