The global oil market’s ability to withstand another major supply disruption is far weaker today than it was just a few months ago. That is the main conclusion of a new analysis by the International Monetary Fund (IMF), which warns that the mechanisms that helped contain the impact of the conflict in the Middle East are now “virtually exhausted.”

According to the IMF, more than 1.1 billion barrels of oil failed to reach the market between March and May—roughly the equivalent of 10 days of normal global oil consumption. Despite that massive disruption, the global energy system avoided a supply crisis thanks to three key factors: weaker demand, increased production outside the Persian Gulf, and the large-scale use of commercial inventories and strategic petroleum reserves.

For transportation, logistics, and freight companies, the message is clear: the system absorbed one major shock, but doing so again will be much more difficult.

The Safety Cushion Has Nearly Disappeared

The IMF explains that the global economy was able to absorb the initial disruption because many countries drew heavily on their strategic petroleum reserves, while producers such as the United States, Guyana, Venezuela, and Russia increased output to offset part of the shortfall. At the same time, higher oil prices reduced demand in several markets, particularly across Asia.

That margin of safety has now largely disappeared.

According to the IMF, spare capacity has been used, inventories have fallen, and demand is unlikely to decline much further without slowing economic activity. As a result, any new major supply disruption would likely have a far greater impact on global oil prices and fuel availability.

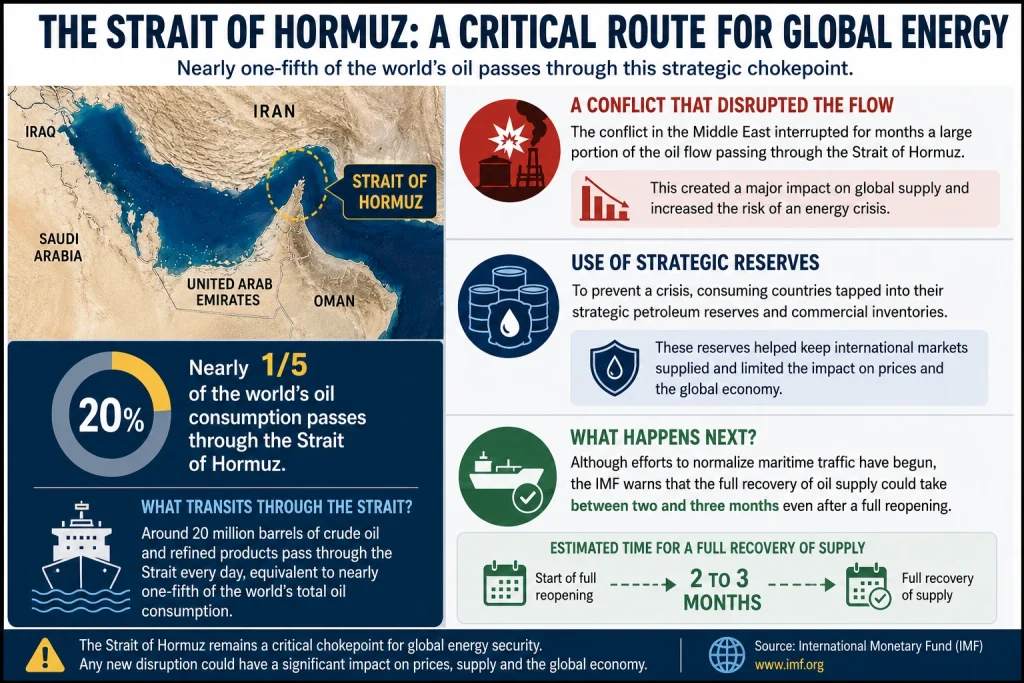

The Strait of Hormuz Remains the Biggest Risk

Much of the concern centers on the Strait of Hormuz, through which nearly 20% of the world’s oil supply normally passes.

The conflict in the Middle East disrupted a significant portion of that flow for months, forcing countries to rely on strategic reserves to keep global markets supplied. Although efforts to normalize maritime traffic have begun, the IMF warns that restoring normal supply levels could still take two to three months, even after a full reopening.

For the logistics industry, this means fuel market stability continues to depend on an infrastructure corridor that remains highly vulnerable to any geopolitical escalation.

What Could This Mean for Transportation?

Oil prices affect far more than the cost of diesel.

When energy markets come under pressure, transportation costs by road, sea, and air typically rise. Cargo insurance premiums increase, delivery times become less predictable, and the availability of certain goods can be affected.

The IMF warns that the world is entering this new phase with fewer tools available to cushion another energy shock. As a result, any additional disruption could quickly spread throughout the global supply chain.

For transportation companies, this could mean:

- Greater volatility in diesel prices.

- Higher operating costs.

- Changes in freight rates.

- Delays in fuel and cargo deliveries.

- Increased uncertainty when planning long-term operations.

Three IMF Recommendations

The IMF outlines three priorities to reduce vulnerability to future energy crises.

The first is to rebuild the strategic petroleum reserves that were heavily used over the past several months, as they remain the world’s primary safeguard against major supply disruptions.

The second is to diversify both energy sources and supply routes, reducing dependence on critical chokepoints such as the Strait of Hormuz. The IMF also notes that improvements in energy efficiency and the continued growth of renewable energy helped soften the initial impact of the conflict.

The third recommendation is that government support measures to offset higher fuel prices should remain temporary and targeted, avoiding market distortions that discourage energy conservation or place additional strain on public finances.

A Warning That Also Applies to Logistics

Although the report focuses primarily on the global oil market and the broader economy, its conclusions have direct implications for the transportation sector.

Companies that rely on fuel to move freight should prepare for a market in which volatility could once again become the norm. Closely monitoring energy markets, optimizing route planning, and maintaining strict cost control will become increasingly important to reduce operational risk.

The IMF concludes that the global economy successfully weathered the first major shock of the Middle East conflict, but only because extraordinary resources were available at the time.

Those resources are no longer available on the same scale. If another significant disruption to global oil supplies occurs, the world’s ability to respond will be far more limited—and the effects could quickly ripple across the entire transportation and logistics industry.