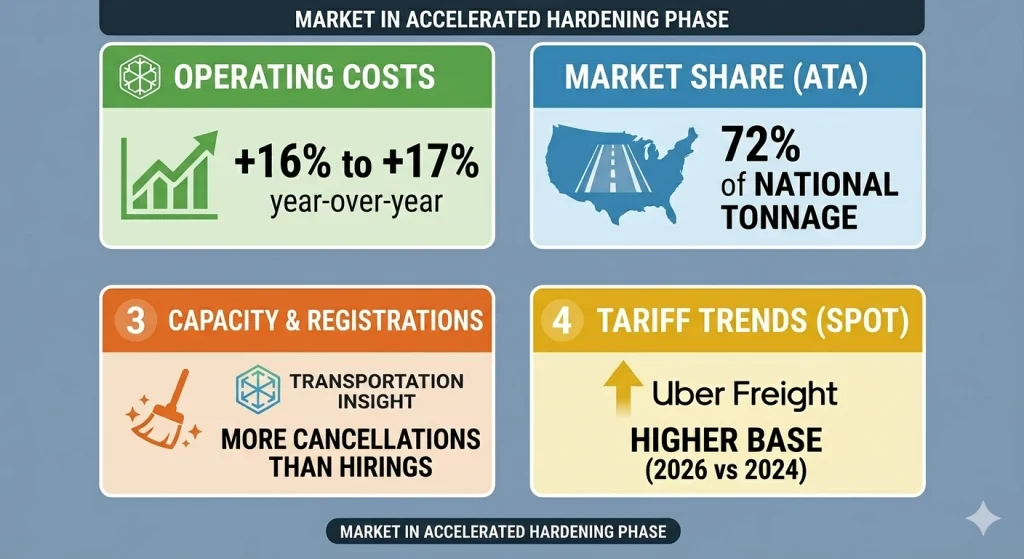

The U.S. freight market has finally broken its downward trend of recent years and entered a phase of accelerated hardening. After experiencing one of the longest and most severe recessions in recent history, trucking rates are now registering significant increases driven by a real contraction in supply. According to the April 2026 report by logistics firm C.H. Robinson, operating costs are now projected to grow year-over-year by 16% to 17%, marking a decisive turning point for the financial health of carriers.

This dynamic is a direct result of the decline in installed capacity, as the number of carrier cancellations has consistently outpaced new registrations in recent quarters. Transportation Insight experts note that this market “cleanup” is allowing surviving carriers to regain lost bargaining power. Even during periods traditionally considered low seasonal demand, price pressure remains strong because there aren’t enough trucks available to cover critical routes, forcing shippers to accept upward adjustments.

Fewer trucks, better rates

The operational reality for independent carriers has been brutal, but it’s creating the necessary groundwork for a revenue rebound. The American Transportation Research Institute (ATRI) has documented that, although average operating costs per mile showed slight declines previously, the pressure on smaller carriers reached record levels of unsustainability, forcing thousands of trucks off the road. This reduction in supply is the main driver of current rates, as the equipment shortage is now more severe than many industry analysts had anticipated for this quarter.

For its part, the American Trucking Association (ATA) projects that freight tonnage will continue its upward trajectory, estimating that by the end of the decade the sector will move billions of additional tons. ATA Chief Economist Bob Costello emphasizes that the trucking sector continues to dominate the national logistics landscape, representing more than 72% of the total tonnage moved in the country. This structural dependence ensures that, with any upturn in economic activity, the demand for trucking services will quickly outstrip available capacity, driving up spot and contract market prices.

Adjustments and Survival

The recovery is not uniform and requires impeccable financial management from truck owners. Uber Freight reports suggest that contract rates are following a moderate upward trend, while the spot market shows greater volatility but with a much higher floor than in 2024 and 2025.

Carriers who have managed to maintain direct relationships with strategic shippers are capturing the best margins, taking advantage of the fact that companies are seeking to secure capacity in advance to avoid the cost spikes expected for the upcoming peak season.

Despite this favorable revenue outlook, external challenges such as diesel prices and insurance remain critical factors. Institutions like ACT Research warn that margin recovery could be “non-profit” if per-mile costs are not controlled with the same rigor as freight negotiations. Therefore, process digitization and route optimization have become essential tools to maximize the return on every mile traveled in this new market cycle.

The outlook for the rest of the year is clear: the market has shifted in favor of the carrier. The combination of a still-demanding consumer goods economy and a leaner, more efficient national fleet has created the perfect scenario for a sustained recovery in fares. Operators who manage to navigate fuel volatility and keep their fleets on the road are best positioned to capitalize on this cyclical shift, which, after years of anticipation, finally appears to be here to stay.

Beyond freight rates, this upward trend coincides with the overall stabilization of the U.S. economy, where moderating inflation and steady consumer demand are restoring balance to the supply chain. After months of market fluctuations, the stabilization of freight volume provides a solid foundation for trucking companies’ operations.

Industry experts note that this phase of economic slowdown does not indicate a slowdown, but rather a healthy recalibration that allows trucking rates to remain at a sustainable and profitable level going forward.