How Is Practical Miles Pay Calculated Compared to Map Miles?

Understanding the difference between Practical Miles, Map Miles (HHG), and Hub Miles can make a significant difference in a driver’s pay per mile.

Flock Cameras Under Fire Over Police Spying

Flock cameras are part of a network of more than 120,000 devices that read license plates and help recover stolen vehicles and cargo. But they can also be used to spy. The controversy is growing.

Leasing, the master formula to beat high interest rates

Independent owner-operators are choosing to upgrade their trucks without depleting their capital. This is how they are coping with the stifling effects of traditional loans and stringent environmental regulations.

Texas: What Happened to the USPS Driver Found Dead Inside His Mail Truck?

OSHA is investigating the death USPS driver who was found unconscious during an extreme heat event in Texas.

Freedom Haulers: How Veterans Can Get CDL and Start a Trucking Career

The Trump Administration’s new Freedom Haulers initiative connects military veterans with commercial trucking jobs through paid CDL training, GI Bill education benefits, military driving waivers, and direct access to employers.

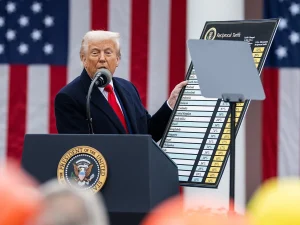

More Tariffs? New U.S. Trade Measures Target 60 Countries

President Donald Trump is set to launch a new round of double-digit tariffs on imports from 60 countries.